作者大約簡略的討論到了巴菲特的合夥人查理蒙格(Charlie Munger)在他的Wesco Financial公司裡討論到了計算一間公司的內涵價值(Intrinsic Value).

計算intrinsic value沒有一個特定的方式, 因為每間公司都不一樣.

許多人說Wesco Financial是一間小的Berkshire Hathaway (巴菲特與蒙格的傑作),但Munger自己也說道這想法是不對的. Berkshire是一間更優異管理團隊及企業文化的公司,且擁有的旗下公司都是首屈一指的.

文章裡說道,不同於Buffett, Munger在1997-1999的Wesco股東信裡面都有提示其中幾個計算內含價值的方法 (因為我還沒時間唸到Wesco Financial 的信, 不過那是必念的所以過段時間唸完有筆記會在post上來.)

在這邊先提到一個intrinsic value(內含價值)的side note

同於巴菲特在年輕時的Buffett Partnership(巴菲特合夥人)的股東信裡,他有介紹到如何去計算內含價值, 蒙格在這邊也是將資產負債表(Balance Sheet)裡面的資產一樣一樣的解析...並自己給予那些資產一個個人認定的價值. 這可能聽起來有點複雜,但是其實這靠的就是經驗跟一些基本的知識. 例如,當一間financial holding公司的資產多為股票組合,債券,和現金時,那他的book value就更能反應出它的內涵價值.

但若一間retail公司的資產擁有大量的貨品跟機器,那當分析它所擁有的資產時最好是給個折扣(discount). 若要保守估計, 例如你可以給把equipment 以 30%來計算 (純粹舉例),然後整間公司折扣過後若還遠遠高於價值,那你的安全邊際(margin of safety)也就相對的高. 不過別忘記注意那間公司的獲利能力, 有可能它也一直在燒錢.

回到Charlie Munger在Wesco Financial的股東信.

因為Wesco這間公司已經似於Berkshire, 資產多為併購的公司,現金,及股票等極度liquid的資產. 且也不亂放dividend或發行股票來稀釋股票,造成難以計算整間公司的價值. 所以Wesco的book value其實算是一個跟其他上市公司比起來"相對" 準確,好計算,且保守的指標.

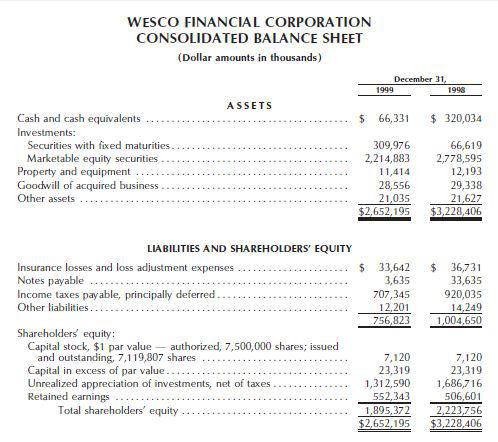

所以像這文章作者提到的,Wesco的財務報表:

在這邊看到1999年的 Book Value Per Share (每股的帳面價值) 為 (股東權益/股數)

$266 = 1,895,372,000 / 7,119,807

可是注意到,其中的債務(Liability)表裡面有一個叫作 (Income taxes payable, principally deferred)的項目. 那叫做Deferred Tax (中文應該叫遞延稅項), 會計在這邊計算成負債. 重點是, 這債務是Wesco欠政府的還沒付出去的稅款, 而這約$7億美金的稅款可能會欠到許多年後才到政府手中. 為什麼會有這大筆的deferred tax liability? 跟波克夏Berkshire Hathaway一樣, 他們手中握有的許多股票上漲了以後, 會產生一筆稅, 但這筆稅卻在你賣掉資產以前是不會被要求支出的! (見下面的圖)

所以往另一個方向看,這其實就像"免費的資金", 或換句話說, 像Dell戴爾電腦的營運資金, 或像保險公司的float (浮額金). 類似這樣的情況會有很多種, 且有些deferred tax根本就不該被認為資產, 所以這一切都應該要靠 - 經驗跟跟一些商業知識來判斷 (或Google). 會計是一商業的學問,所以我自己也還在不斷從書籍跟網路學習. 若唸的懂英文的朋友, 我常常從 investopedia.com 上面學習某些知識.

這可能對初階者來講有點複雜, 不過總而言之, 就是本應該屬於別人的資金, 但卻讓你免費(無利息)的持有運用許多年, 所以某些部分來說應該要被當成"資產"而非債務!

Deferred Tax Table:

所以每股的deferred tax大約為$99美元:

$99 = $705,343,000 / 7,110,807

但是Munger也說道:

_____________________________________________________

However, some day, perhaps soon, major parts of the interest-free "loan" must be paid as assets are sold. Therefore, Wesco's shareholders have no perpetual advantage creating value for them of $99 per Wesco share. Instead, the present value of Wesco's shareholders' advantage must logically be much lower than $99 per Wesco share. In the writer's judgment, the value of Wesco's advantage from its temporary, interest-free "loan" was probably about $20 per Wesco share at yearend 1999.

粗體部份的翻譯:

但是,某一天,可能很接近,大部份的這些"零利息的資金"需要付出去. 所以這些資金的價值對Wesco股東來說沒有永久的價值. 所以我們可以合理的判斷說那價值應該低於$99美元. 對作者來說, 這筆資金的價值是暫時的, 所以這比零利息資金的價值在1999年底應該約為$20.

_____________________________________________________

那所以帳面價值, 剛剛上面計算的 $266, 加上蒙格給deferred tax這個資產(帳面上稱作債務) $20元的價值. 所以保守估計這間公司1999年的價值約為$286.

價值應該為$286還$300這都不重要,因為價值的判斷因人而異. 重點是在了解完一間公司後能不能有信心的判斷這公司的價值遠低於價格.

這也告訴我們, 一間公司要是像2007年的AIG一樣或許多其他公司擁有極為複雜的報表, 有可能是管理人根本不想你看的懂,或你也無法了解這間公司. (Ironically,我現在擁有AIG) 那你可以去找更容易理解的公司來分析, 這樣你也相對可以有更高的margin of safety, or 安全邊際.

有問題歡迎請教

Cheers!

(歡迎分享這個Blog及留下意見)

8 則留言:

Great post! Negative working capital / Insurance float / deferred tax liability are great examples of interest-free loan. I agree AIG is dirt-cheap... Bruce Berkowitz's top holding. well. less cheap now. Check out its TARP warrant for a levered play.

Yes and I am glad to see people who also follow the US equities to chime in. Thanks for commenting.

I invested in AIG after following several value investors and particularly after reading Whitney Tilson's presentation.

It's screamingly cheap, but I am among one of those who thinks AIG might be selling ILFC too cheaply...?

Benmosche mentioned they might be leaving money on the table... but they need the cash for buybacks. The deal may not go through anyway. The initial deposit was late.. so who knows? It may fall through and they may do an IPO on it instead.

Hey I apologize for the late reply. I need to look around and see if Blogger has notification on comments.

I am not so worried about ILFC, however, I do have a concern about its asset...

AIG holds about $246 billion of available for sale fixed income securities, and $100 billion of those are due after 10+ years. Although I am not clear on what the yield on those assets are, I suspect they are at the high range. With interest rate/inflation destined to rise, any drop in fair value of its debt holdings will wipe out the equity value easily.

I don't know what a equity wipeout would mean to a company. I think it's not affecting AIG's earning generating operations. But it's still a risk.

I emailed Whitney Tilson since he prepared an AIG presentation. He thinks it's a huge upside for all insurance to have interest rate rises. I know it's an upside, just I dont know how to measure the downside of the case I just described above...

And apologize for this long reply. It may be easier for us to talk on fb chat :P

pasted my message from FB:

RE: AIG

just saw ur reply

yeah, interest rates sure going to rise, but higher durations get hit first...

10+yr bonds presumably have higher coupons(which lowers duration) and ought to dampen higher duration of the par maturity impact. I would say it's more like a push.

as bonds mature, they can re-invest in higher yield bonds.

Banks have similar problems. Higher yield would kill their existing portfolio, but at the same time raise mortgage coupons and Net Interest Margin.

I also heard Benmorche were looking to underwrite mortgage or some sorts to generate their own yields.. anyway, that's off topic

no way to get around bear-market in bonds.

in any case, I think AIG is a sell around book value unless you are excited about the subsequent 10-15% return.

Hey MC

I read this article a while ago too: http://www.cnbc.com/id/100843724

Like I brought up to you last time, I emailed Whitney Tilson and he told me that a rise in interest rate is a big PLUS for AIG. I understand the long-term benefit that a rise in interest rate would do to an insurance or other financial service companies like AIG.

Just wondering the near-term hit on its balance sheet fair value...since it's wayyyyy larger than the current equity and market cap, would kill the company. I don't think it will. Just wondering the risk here.

Obviously the analysts quoted in CNBC is aware of the "near-term hit vs. long-term plus" and seems like none of them have a clear view of what the rise of rate would do to the 'available for sale' on the banks.

Perhaps I am worrying too much. The upside is certainly wonderful.

A research data about AFS I found from the CNBC article is: http://research.stlouisfed.org/fred2/series/NUGACBM027NBOG

Have a great weekend man and thx for the papers.

I'm heading up to TPE now.

Whitney Tilson actually replied you? That's very nice of him. I wouldn't think it would be a big plus though.

yeah, fair-value of the AFS debt holdings would be hit. no doubt... but funny thing about GAAP, fair-value hit on the AFS holdings would pass through AOCI (Accumulated other comprehensive income) and reduces the equity, but does not reflect in the net income in terms of write-downs. HTM loans would not be hit since they are marked at cost I believe.

I know it makes no economic sense, but it's how GAAP works. And I believe it applies to insurance companies as well. The equity value would likely be hit... which ironically could exaggerate ROE a bit.

Also you may want to keep in mind that liability side could also be reduced as future insurance payouts are discounted more by higher yields.

Banks benefit from a steep yield curve. i.e. They borrow short-term (via deposit or some other short term financing) and invest the proceeds in longer term holdings such as mortgages, commercial loans, muni bonds... The net interest margin actually helps in a rising interest rate environment. I know WFC used to make 5-6% in NIM.. now it's more like 3.5%. Banks have tremendous earnings power on the upside.

Yes the AFS debt wouldn't hit the income statement, and my opinion is that a mere equity wipeout shouldn't affect the real earning power of the business.

Yeah the discounted payout is a good point, thx for pointing it out. I agree on the NIM side, and WFC is a very different bank. Not just cuz it's US centered but John Stumpf looks at it more as a community bank as well. They are going to push the credit card to homeowners too since only a small percentage of customers have WFC for now. I'm adding the twitter accounts now..there are quite a few. thanks a lot!

張貼留言